Printable Version of Topic

Click here to view this topic in its original format

914World.com _ 914World Garage _ Insurance: classic vs. antique vs. standard

Posted by: JerryP Feb 26 2004, 12:31 PM

Anybody use classic or antique insurance? I'm in PA with a '72 2.0. Grundy Worldwide says no coverage going to school, work or on errands. Anybody know the pro's and con's of this insurance? I want to know if I should dump my standard insurance and save about 75%. I don't use the car as a commuter but I would like to be covered if I get spanked by a Buick in the Home Depot parking lot. Ideas? Thanks.

Posted by: seanery Feb 26 2004, 12:34 PM

That coverage wouldn't do it for me. I like to USE my car. It sounds like you are covered only during pleasure drives and car events. Not enough coverage for me.

Posted by: tat2dphreak Feb 26 2004, 12:35 PM

http://www.hagerty.com/vehicle_index.asp?Aff=

I've heard great things about them, and plan to use them when my car makes it's triumphant return to the roads!

Posted by: seanery Feb 26 2004, 12:44 PM

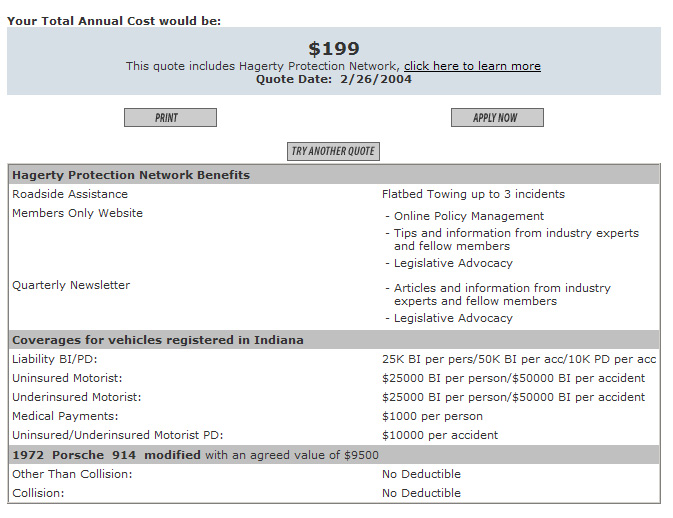

this is what Hagerty said about insurance for me:

what's wierd is they didn't ask for any personal info about me

Attached image(s)

Posted by: tat2dphreak Feb 26 2004, 12:57 PM

I know... that's weird, but they assume a clean driving record, and won't insure you without a clean record... they do limit miles, but it's not very restrictive... something like 7K miles per year... I only put 10K on my daily driver per year! and the 914 will not be a daily commuter car...

Posted by: seanery Feb 26 2004, 01:01 PM

7k a year is no problem. I'm sure between both cars I don't even do 10k a year now (unless I drive to LA or SF in one)

Posted by: seanery Feb 26 2004, 01:07 PM

I just called my SF agent to ask them about Hagerty. I gave her the #s listed above, they are the bare minimum state levels of inssurance.

Posted by: tesserra Feb 26 2004, 01:10 PM

Hagerty is a good company to support.

They have "scholarships" for old car restoration. They support restoration and feel that a car sent to the junkyard smasher is a piece of history, and potential premium, forever lost.

They insure my Woodboat and have a great approach to classic vehicles.

George

Posted by: JerryP Feb 26 2004, 01:11 PM

I used 6500 as agreed value and got a $90 per year premium with Hagerty. Grundy has a 2500 mile/year limit on classic insurance. If 7k is correct and you can drive at night, I'm in. Thanks guys.

Posted by: tat2dphreak Feb 26 2004, 01:14 PM

call them to double check about the milage limits, I'm going by what a friend heard... but I'm sure it's more than 2500 miles! that's Nuckin' Futs!

but I've known a few people use hagerty... I would err on the side of caution... assume you are going to have to buy another 914 if you wreck this one... I allowed for 12K... if they only agree on 10K... you are still in decent shape.

Posted by: seanery Feb 26 2004, 01:16 PM

double check that your coverage is adequate-those #s were too low if you caused a serious accident....I know, we never think it could be our fault, but it could...

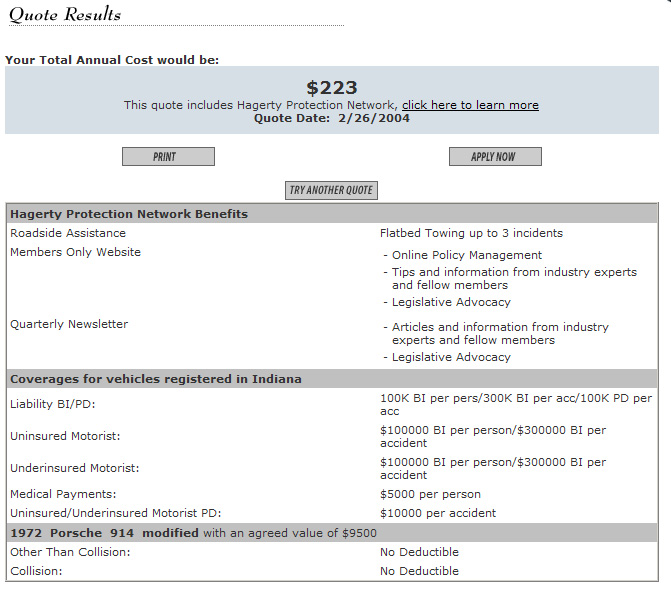

Posted by: seanery Feb 26 2004, 01:41 PM

I bumped up the coverage #'s (you have to do that manually) to get them closer to my State Farm coverage.

This is what I got, still, it seems like a good deal.

Attached image(s)

Posted by: seanery Feb 26 2004, 01:52 PM

I just got off the phone with them.

1.They like to see mileage ~2500/year for the car

2.Driving to the grocery and it gets hit is OK, but they would rather you not drive it to/from work and for chores, etc...

3.They need a pic of each car to insure

4.They need a copy of your daily driver car's insurance policy.

5.Yearly premium to be paid in full.

I think that's about it. Sounds like a decent price and deal to me.

Posted by: JerryP Feb 26 2004, 01:54 PM

cool...I didn't see that you could manually change the coverage on their website. I did just call Hagerty though and they told me they are not concerned with actual mileage as much as how the car is used. They only write you a policy if there is already one car for every driver in the household.

Posted by: seanery Feb 26 2004, 01:57 PM

I forgot two more things:

1. Driving from IN-SF for West Coast Classic is ok, no problems with the 4200 miles

2. They will insure a race car-not while it's on the track, but during storage and travel.

Posted by: tat2dphreak Feb 26 2004, 02:34 PM

so it's the car's "use" more than the mileage... that's a hell of a deal if you ask me! I only will drive around (sonic on Saturdays  ) and maybe occasionally to work or to MUSR or parents house(300 miles) I'd be shocked if I put 2.5K on in 1 year!

) and maybe occasionally to work or to MUSR or parents house(300 miles) I'd be shocked if I put 2.5K on in 1 year!

Posted by: RustyWa Feb 26 2004, 02:49 PM

When I talked with Hagerty....they said they did not like you using it for errands or driving it to work. That was enough for me to pass on them. Sounds like depends on the agent you talk with, might get different answers.

Posted by: ninefourteener Feb 26 2004, 02:54 PM

I have dealt with this..... and I chose to go with just "regular" full-coverage. There's no mileage restriction, and with classic insurance... they said that the car has to be either in a garage, or in plain site, at all times.

That means if I go to Wal-Mart to pick up toilet paper in the teener, and someone smacks into me, I'm not covered because I wasn't actially "watching" the car.

The downside? If I total it, they will not want to cover the entire value of the car.... which means I may have to take them to court. Thats why I have an in-depth video of the car, and two different appraisals at $9000, and $9600 respectively. I highly doubt I'll total it.. I drive it like grandma, especially with my daughter in the car.. so I think I'll be ok.

The upside?? I have full coverage on a 2002 Acura RSX, and full coverage on a 72 2.0. I have towing, rental reimbursement on both, and I'm a 28 year old single male....... I pay about $110 a month.... not too bad

Just my 2 cents

Posted by: DuckRyder Feb 26 2004, 03:22 PM

You do realize that SF writes a "Collector Car policy" (At least in most States)

Watch "Stated Value" policies, they are not always "Agreed Value". If you buy an agreed value policy the declarations page should say some thing like:

"Vehicle value is 9500.00" - "Limit of Physical damage coverage is 9500.00"

If it says something like:

"Estimated vehicle value is 9500.00, settle on ACV"

The estimated value won't do you much good, but the company will charge premium based on it.

Now, about the limits:

[RANT on]

Riding around with minimum limits this day in age is absolutely foolish. I would not leave the house in anything without 100/300/100 limits AT LEAST! All my stuff has 500,000 single limits.

One little lapse in attention or misjudgment could ruin your entire life. You could quite accidentally be involved in an incident and get a hundreds of thousands of dollars judgment against you, seen it happen too many times, Trust me, it'll be bad enough mentally and physically without the added stress of how you are going to pay the $275,000.00 excess judgment.

[RANT off]

Posted by: tat2dphreak Feb 26 2004, 03:46 PM

1st off... on the "usage" it's not like you have to tell them WHERE you were going or what you were doing when it happened... if you ask them, then yes, they will care if you use it for going to work... because they will assume that you will do that often... if I get smacked in a parking lot while getting a quick thing and they ask... just say "I was having one of my rare drives and I remembered I was out of flour tortillas, so I decided to stop off..."

hagerty does have to agree on how much you are covered for... that way someone can't insure a Pinto for 20K and get a brand new car from the deal. the tool on the web is just to give you an idea...

ninefourteener... I think you misunderstand... the $120 hagerty quotes is for a YEAR... not a month... but 110/month is not bad at all... I had my Chrysler(POS), my wife's Civic, and the old teener on and with reneters insurance... it was $150..

35 of which was the teener... 35 *12= 420 /year that is why I am going with the hagerty... I don't drive it enough to warrant $420/year

it's not bad, and if you can afford it, have both!!! THAT is the way to go!

Posted by: Justin Fischer Feb 26 2004, 04:07 PM

Watch "Stated Value" policies, they are not always "Agreed Value". If you buy an agreed value policy the declarations page should say some thing like:

"Vehicle value is 9500.00" - "Limit of Physical damage coverage is 9500.00"

If it says something like:

"Estimated vehicle value is 9500.00, settle on ACV"

The estimated value won't do you much good, but the company will charge premium based on it.

Be careful with SF, I'm insured with them, I set up an Agreed Value policy with them, and then after hearing some SF "Agreed Value" horror stories, I called and starting asking questions again. After 10 minutes of giving me the run around he says: "Well technically, we don't do "Agreed Value" policies, but we'll check the market, and fight to get you as much money as we can if something happens to your car."

Maybe SF does them some places, hell, my agent told me mine was for two years. CYA.......

Posted by: seanery Feb 26 2004, 04:47 PM

After talking with Hagerty, especially since they'll insure the race car. I'll switch to them. For me to insure both cars and have the highest limits they do (see my previous pic #2) was $420/year and that listed the -4 at $10,000 and the race car at $15,000. I know I've more than that in the race car, but that's what it would probably sell for in it's current condition (IMHO).

Posted by: DuckRyder Feb 26 2004, 05:53 PM

Watch "Stated Value" policies, they are not always "Agreed Value". If you buy an agreed value policy the declarations page should say some thing like:

"Vehicle value is 9500.00" - "Limit of Physical damage coverage is 9500.00"

If it says something like:

"Estimated vehicle value is 9500.00, settle on ACV"

The estimated value won't do you much good, but the company will charge premium based on it.

Be careful with SF, I'm insured with them, I set up an Agreed Value policy with them, and then after hearing some SF "Agreed Value" horror stories, I called and starting asking questions again. After 10 minutes of giving me the run around he says: "Well technically, we don't do "Agreed Value" policies, but we'll check the market, and fight to get you as much money as we can if something happens to your car."

Maybe SF does them some places, hell, my agent told me mine was for two years. CYA.......

What does your declarations page say?

Posted by: ldino21 Feb 27 2004, 05:50 PM

Realize that a Hagerty Insurance policy requires that the vehicle to be insured is not your primary vehicle and that you have insurance on your Primary vehicle. They ask for company and policy number.

If this is the case for you Hagerty is a great Classic Car policy, it is not too limiting, you can put how much mileage you are actually driving the car.

If you need more info let me know!!

Lou Smaldino

Smaldino Insurance Agency

Posted by: ldino21 Feb 27 2004, 05:56 PM

With regards to Stated Value policies:

If you buy a stated value policy you need to make sure that your Stated Value is correct. Anyone can walk into an office and say I want a $20,000 Stated Value policy on my Ford Pinto and some agent might sell it to you, but that doesn't mean you are going to get $20,000 if that car gets mysteriously stolen or something.

With every insurance policy in California, YOU need to be able to prove the value of your vehicle, the best way to do this is to get an APPRAISAL!!

Pictures, receipts and Service Records help, but an Appraisal is better!!

An appraisal is considered a disinterested 3rd party when it comes to settling up with an insurance company, and it usually gives a pretty acurate value. Most Body shops, or Dealerships can point you in the direction of a good Appraiser.

Good Luck

Lou Smaldino

Powered by Invision Power Board (http://www.invisionboard.com)

© Invision Power Services (http://www.invisionpower.com)